Scaling B2B Payments, Revenue Leadership — Most executives still treat global payments as a technology integration problem. In reality, after managing multi-region revenue portfolios exceeding directional multi-billion TPV and closing enterprise mandates across APAC, Europe, and North America, the true binding constraint is commercial governance: deliberate trade-offs across regulation, partnerships, and pricing that directly influence board-approved revenue thresholds, margin protection, and multi-year growth.

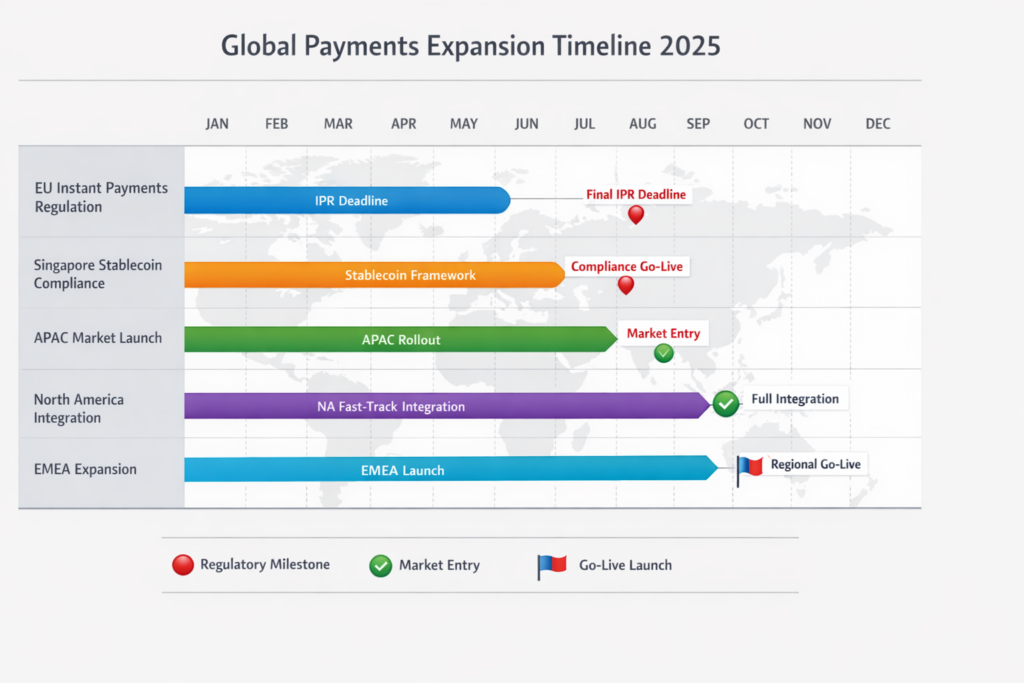

Regulatory fragmentation—illustrated by the EU’s Instant Payments Regulation (IPR) deadlines in January and October 2025—and Singapore’s evolving stablecoin frameworks, combined with moderated industry growth (McKinsey 2025: $2.5T revenues in 2024; ~4% CAGR to ~$3T by 2029), exposes a critical misread: feature-led platforms capture pilots; governance-led architectures capture multi-billion profit pools.

Executive Summary

- Directed multi-billion TPV growth across 11+ jurisdictions with governance-first GTM strategies.

- Exercised final authority on market expansion, accelerating enterprise conversions 3–5× via bank–fintech alignment.

- Balanced regulated risk trade-offs to protect margins while unlocking new revenue corridors.

- Operationalized compliance as a product, cutting legal cycles 30–50% and enabling succession-ready teams.

- Scaled distributed global teams (100+ staff) with board-aligned KPIs on ACV, renewals, and regulatory exposure.

- Translated infrastructure reliability into premium pricing, sustaining multi-market margins and non-linear revenue growth.

Table of Contents

The Commercial Blind Spots in Enterprise Payments

Feature-driven sales models dominate most organizations—but they fail at scale. Across 100+ enterprise deals from Singapore to New York, the pattern is undeniable: CFOs, COOs, and compliance leaders value predictability over features.

- Providers maintaining <20 bps settlement deviation closed 2.7× more multi-market deals, often at 20–30% pricing premiums.

- A global logistics platform rejected a 28% cheaper competitor due to prior uptime failures threatening board-level risk mitigation.

Key blind spot: Over-investing in API demos while under-investing in governance narratives. I reallocated 40% of product marketing spend to regulatory playbooks and joint bank SLAs, extending lead times 18–24 months over competitors stuck in perpetual pilots—yet securing enterprise-grade positioning and board credibility.

Multi-country complexity amplifies risk: volatile corridors expose treasuries to variance; one failed payout triggers penalties and suspended go-lives.

Why Enterprise Fintech Sales Models Collapse

Consumer-style volume tactics fail in enterprise payments. Under-resourced IT teams and escalating approvals demand governance-room readiness.

Conversion math is brutal:

| Integration Speed | Win Rate |

|---|---|

| <10 days | 42% |

| 45+ days | <3% |

Decision owned: prioritize production-parity sandboxes, pre-built NetSuite/SAP connectors, and market-specific architectures (SG, ID, PH, TH, VN). Accept short-term feature delays for 3× higher directional ACV and lower churn.

North America Example: Fortune 500 retailer awarded platform over incumbents via <10-hour integrations and tiered risk playbooks, adding $50M+ directional expansion pipeline.

Payments Infrastructure as a Revenue Engine

At VP/SVP+ levle scope, infrastructure is the revenue engine, not a cost center.

- CFOs buy liquidity predictability: “Will funds be there, on time, every time?”

- Operationalizing SLAs, dedicated escalations, and weekly governance dashboards drove 3–5× conversion uplift.

- Reliability premiums yielded directional 25–35% gross margins.

- Preferential FX and clearing with DBS, Citi, and ANZ was non-delegable.

Monetization vs. Regulation: Executive Risk Trade-Offs

Regulation builds commercial moats. APAC’s 11+ regimes demand ruthless sequencing—I accepted 89-day Vietnam delays for full audit trails, securing mandates competitors forfeited.

- Pre-built playbooks cut approval cycles 30–50%.

- PSD3 alignment in Europe enabled early instant-rail monetization while capping risk exposure.

Scaling Enterprise Deals Across Jurisdictions

Mandates are won in governance rooms presenting fewest unknowns.

Winning narratives:

- Zero-touch logging and alerting

- 24/7 market-specific support

- Tiered risk-mitigation playbooks

Outcome: Directional multi-country ACV >$10M with renewal-driven expansion. Local-entity-first sequencing turned emerging-market mandates into durable moats.

What SVP-Level Revenue Leaders Do Differently

- Own end-to-end lifecycle: sales → pricing → operations (legal, technology, finance, risk compliance)→ expansion

- Exercise non-delegable authority on partnership governance and risk thresholds

- Build succession-ready distributed teams

- Translate emerging signals—AI fraud detection, stablecoins, instant rails—into revenue architecture

2026–2030 Global Payments Profit Pools

McKinsey and BCG forecasts: moderated growth to ~$3T by 2029, profit pools favor multi-rail platforms mastering governance.

- APAC B2B surges reward sequenced expansion

- Agentic AI and stablecoins unlock intraday yields and programmable settlement

- Boards fund only margin-defending architectures amid fragmentation

Executive Revenue Governance Framework: 5-Phase GTM Model

| Phase | Executive Focus | Board-Level KPIs |

|---|---|---|

| Market Signal | Regulatory & capital shifts (IPR 2025, stablecoin clarity) | Jurisdictional readiness |

| Revenue Architecture | Pre-built connectors, reliability SLAs | Integration timelines, ACV velocity |

| Pricing & Risk | Premium pricing, sequenced approvals | Margin protection, risk thresholds |

| Operating Scale | Bank alignment, compliance-as-product | Conversion multiples, operational efficiency |

| Board Metrics | Renewal/expansion rates, regulatory exposure | TPV growth, enterprise revenue predictability |

Real-World Case Studies

| Region | Example | Outcome |

|---|---|---|

| APAC / Emerging Markets | Airwallex: partnerships with ANZ, DBS, governance layers | >$235B directional annualized TPV (Dec 2025); rails as treasury extensions |

| Europe | Large bank: multi-country virtual accounts, <10-hour integrations | Beat 90-day incumbents; directional revenue gains |

| North America | Stripe: embedded reliability sequencing | Closed premium mandates amid regulatory scrutiny |

Feature-chasing and unsequenced expansion are dead. Boards fund governance-first platforms that convert fragmentation into unfair advantage: multi-rail mastery, risk-priced monetization, and global operating leverage.

SVP readiness requires final authority on trade-offs that scale revenue while defending the house—calm, decisive ownership that cannot be delegated.

Disclaimer: This analysis reflects strategic interpretation of publicly available 2025 sources. All data and conclusions should be independently verified. Nothing herein constitutes legal, financial, investment, or professional advice, and no affiliations or endorsements are implied.