Multirail payment ecosystems are becoming the new operating system of global fintech as CXOs move beyond single-rail dependencies. Bold as many legacy-treasurers and CFOs may be, the era of a single dominant payment rail is over — and the real battleground will be defined by orchestration, not dominance. Real-time account-to-account (A2A) systems, diverse rails (cards, open-banking APIs, digital wallets, RTP networks) and AI-powered orchestration layers are converging. Boards that assume “cards + SWIFT = safe” are dangerously wrong. Here’s why most boards are getting this dangerously wrong — and what the top 1% are doing instead.

Executive Summary

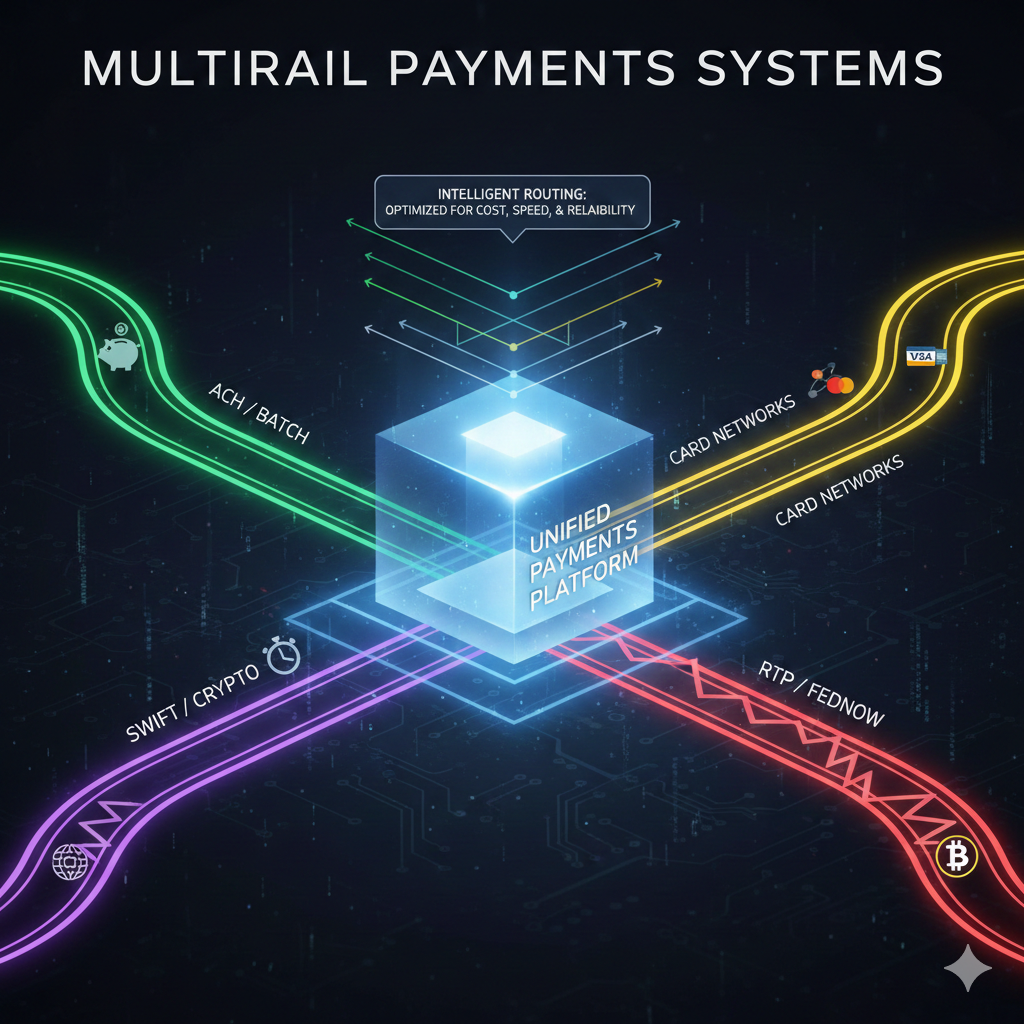

Understanding Multirail Payment Ecosystems

- Multirail convergence: A2A, real-time, cards, wallets — payment flows are fragmenting; orchestration is becoming the strategic asset.

- A2A explosion: Real-time A2A is growing globally — >70 countries now support RTP; volumes to double by 2028.

- Cost & speed advantage: A2A/instant rails threaten 15–25% of future card-transaction growth globally.

- Interoperability as growth lever: True value lies in cross-rail and cross-border interoperability; fragmentation is the principal bottleneck.

- AI-driven orchestration rising: AI routing and orchestration significantly reduce payment failures and improve efficiency.

- Compliance & risk as strategic constraints: Regulatory, liquidity, FX, and fraud-management complexity demand re-architecting.

Table of Contents

The Hidden Market Force Most Boards Are Ignoring

What too many boards dismiss as “alternative payments noise” is actually the fastest structural shift in payments since the birth of card networks.

- In 2023 alone, there were 266.2 billion real-time payments globally, representing a 42.2% year-on-year increase.

- By 2028, real-time payments volume is projected to reach 575 billion transactions per year — more than double 2023 levels.

- In many emerging economies (APAC, Latin America), A2A and instant rails now account for a substantial — and growing — share of retail and e-commerce transactions.

- Meanwhile, legacy card-centric strategies are losing structural advantages: instant rails are faster, cheaper, and increasingly trusted — especially for high-velocity, low-margin flows like gig economy payouts, subscription services, and SME supplier payments.

Boards that ignore this underestimate the risk: not just to payment volume, but to cash-flow dynamics, working capital, and customer experience economics.

Regulatory Tectonics Shifting Beneath Your Feet

Regulation is no longer a backdrop, it’s the accelerator — shaping which rails survive, which fade, and which consolidate.

- In Europe, regulatory pressure under frameworks like PSD2 / open-banking and the newer EU Instant Payments Regulation (2024/886) (VoP requirements, real-time settlement mandates) is pushing banks and payment providers toward instant A2A rails.

- Around the world, over 70 countries now support real-time payments; yet fewer than 50% of payment systems enjoy standards-based interoperability — leading to fragmented rails that don’t “talk.”

- Cross-border payments remain a structural challenge: differing AML/KYC rules, FX regimes, and data compliance (e.g. data localization laws) slow down or block real-time interoperability.

- As geopolitical fragmentation increases (sanctions, data sovereignty, competing CBDC regimes), global payment homogeneity becomes less likely — regional or corridor-based networks look like the more probable future.

Result: Compliance and regulatory strategy must now be central to payment-rail planning — not an afterthought.

The Technology Inflection Point (2025–2028)

Technology — not just regulation or market demand — is now the enabler (or inhibitor) of multirail orchestration.

- API-first, cloud-native architectures are allowing payment-service providers (PSPs) to natively support multiple rails (cards, wallets, A2A, RTP) with a single integration point.

- AI-driven payment orchestration platforms are scaling rapidly: enterprises report up to 38% faster transaction speeds and 27% fewer declines when using smart routing engines.

- Embedded finance — payments built directly into platforms (marketplaces, SaaS, gig-economy, B2B tools) — is accelerating. Real-time rails are becoming the “plumbing” behind embedded credit, subscription billing, and payouts.

- Research into secure, high-throughput settlement architectures (including blockchain-based or hybrid rails) is rising — potentially enabling near-instant cross-border transfers with built-in compliance and traceability.

We are entering an inflection where payments are no longer pipes, but programmable infrastructure — one where orchestration layers, data models, and real-time decision logic determine outcome, not just network access.

Capital Allocation Implications Most CFOs Miss

If you’re still budgeting around legacy card reconciliation, interchange, and correspondent-banking fees — your treasury strategy is already obsolete.

- Lower Cost of Funds & Faster Cash Flow: By routing B2B disbursements, supplier payments, and gig-economy payouts through low-cost A2A rails instead of cards or SWIFT, firms can reduce interchange and FX fees, improve working capital, and shorten cash-conversion cycles.

- Operational Expense Reduction: Multi-rail orchestration reduces complexity — one integration, unified reconciliation — reducing maintenance overhead for PSPs and merchants.

- Strategic Flexibility: Firms that invest in orchestration stacks and open-API layers are better positioned to add future payment methods (wallets, CBDCs, stablecoins) without re-architecting payments — allowing capital to be deployed in product, not plumbing.

- Regulatory Capital & Risk Cost Mitigation: Managing compliance, fraud, AML risks proactively via orchestration reduces unexpected compliance burden — a growing cost as real-time and cross-border regulations tighten.

Boards that treat payments as a back-office cost are missing that payments are now a core capital lever.

Leadership & Talent Re-Architecture Required

Organizations that win will look very different from those that wined under card-led payments era.

- From Payments Ops to Payment Product Management — Teams need product managers fluent in rails, API design, orchestration logic, and compliance regimes, not just ops or treasury clerks.

- Hybrid Technology + Compliance Fluency — Engineers must understand ISO standards (e.g. ISO 20022), encryption/tokenization, real-time data flows; compliance officers must embed risk controls in orchestration logic.

- AI & Data Science for Payment Intelligence — AI-native orchestration, fraud detection, routing optimization; shifting from batch-reconciliation to real-time analytics.

- Cross-Functional Liaison Roles — between finance, product, legal/regulatory, and operations — to manage increasingly global, multi-currency, multi-rail flows.

- Continuous Learning Culture — rails will evolve fast (new instant-payment networks, CBDCs, regulations) — so teams must adapt, not just maintain.

Legacy-first org structures — with payments as accounting afterthought — will be outpaced by agile fintech-style organizations.

Global Case Studies: Proof This Works at Scale

| Region / Company | What They Did | Outcome / Insight |

| APAC – Unified Payments Interface (UPI) / Razorpay (India) | Leveraged UPI A2A for e-commerce, B2C and B2B payments; adopted embedded-payments via fintech platforms. | UPI handles tens of billions of monthly transactions (sub-second settlement capacity), enabling massive digital-economy scale. |

| Europe – SEPA Instant Credit Transfer (SCT Inst) + ACI Worldwide / STET orchestration | Linked national RTP rails under common settlement engine to enable real-time cross-border euro payments. | Processed 50 million cross-border instant payments in 12 months — first real evidence cross-border multirail real-time works at scale. |

| North America / Global – Mastercard Track Business Payment Service (US + global rollout) | Introduced A2A capabilities alongside card payments — giving businesses unified rails for cards + bank-account transfers. | Demonstrates how large incumbents are repositioning as multi-rail payment platforms rather than card networks. |

(Note: for many firms — public financial metrics on cost savings or margins are not available. Directional outcome only. Source: press releases, industry reports.)

The 2026–2030 Profit Pool Map

- Domestic Retail & E-commerce Payments ➝ shifts toward A2A and instant rails in APAC, LATAM, parts of Europe; profitability margin improves due to lower fees and faster cash flow.

- B2B & Supplier Payments ➝ orchestration + A2A lowers working-capital costs and reduces payment friction; cheaper, faster settlements improve supplier relationships.

- Embedded Finance & Subscriptions ➝ real-time recurring A2A + VRP/payment-mandate rails undercut card-based churn; conversion and retention improve (fewer false-declines, fewer failed payments).

- Cross-border SME & Remittance Flows ➝ as multirail interoperability and orchestration stabilise, real-time cross-border A2A displaces expensive correspondent banking and remittance models.

- Platform & Marketplace Payouts (gig economy, marketplaces, global payroll, payouts) ➝ leverage orchestration + real-time settlement to reduce cash-flow risk and improve payout latency.

By 2030, firms that control orchestration — not just individual rails — will command the largest share of payment-related profit pools: routing, FX margins, settlement margins, conversion & retention value, data monetization, and embedded financial services.

CXO Playbook — 5-Phase Multirail Payment Transformation Roadmap

| Phase | Action | Owner | KPI / Milestone |

| 1. Audit & Rail-Map | Inventory all existing payment rails (cards, A2A, RTP, wallets), volumes, costs, failure rates, latency. | CFO & Head of Payments | Full rail-map, baseline cost & latency metrics. |

| 2. Build Orchestration Layer | Implement or partner for a rail-agnostic orchestration platform (with API abstractions, routing logic, reconciliation) | CTO / Ops | Unified payment API, success-rate ≥ 98%, failover logic in place. |

| 3. Compliance & Risk Embedding | Integrate AML/KYC, VoP (verify-payee), FX/conversion logic, liquidity & settlement workflows. | Chief Risk & Compliance Officer | Compliance pass-rate, regulatory audit readiness, liquidity buffer policies. |

| 4. Migration & Rollout | Gradually shift high-volume flows (retail, B2B, payouts) to orchestration + A2A/instant-rail where appropriate. | Product, Ops, Finance | Cost per transaction reduction, cash-flow acceleration, reduction in reconciliation overhead. |

| 5. Continuous Optimization & Innovation | Monitor new rails (CBDCs, stablecoins, new instant-payment networks), integrate AI-routing & future rails. | Product & Strategy | AI-routing success metrics (speed, decline rate), new-rail connect readiness. |

Real-World Proof — Why This Works

- APAC (India, UPI): UPI’s explosion in use — tens of billions of transactions monthly — shows A2A/instant rails can scale to mass-market volumes.

- Europe (SEPA SCT Inst + ACI/STET): 50 million cross-border instant payments in last 12 months, proving real-time, cross-border euro payments via orchestration is not only possible — it’s scaling.

- Global Incumbents (Mastercard Track): By extending its business payments service to include A2A (beyond cards), Mastercard signals incumbents shifting strategies — from “card network” to “multi-rail platform.”

These illustrate that multirail orchestration is not fringe — it’s already delivering real-world value, for consumers and enterprises alike.

The future of payments isn’t about which single rail wins — it’s about who builds the smartest, most flexible orchestration layer. That layer will determine speed, cost-efficiency, compliance, liquidity, and ultimately competitive advantage. Boards that cling to legacy assumptions — card dominance, SWIFT-based cross-border, siloed rails — are not just behind the curve; they risk being structurally noncompetitive.

Pay-rail orchestration is the new factory floor. Own the controller — or become its supplier.

If this sparked new thinking, share your reflections in the comments and repost it for leaders who may benefit.

Disclaimer: This article uses publicly available sources. Information is for general informational purposes only and should not be relied on as financial, legal, tax, or investment advice. Readers should verify facts independently before acting.