Global payments in 2025 are no longer a race for faster rails or broader reach. In 2025, the fintech landscape have matured beyond speed and reach. Real-time rails, APIs, and ISO 20022 are now baseline. The real transformation is structural: innovation redistributes control, margins, and balance-sheet risk—often from incumbents to platforms and fintechs.

For executives, the question shifts from “How do we innovate?” to “Who captures value as payments become invisible, programmable, and embedded?”

Executive Summary

Payments mechanics are converging into utilities. Differentiation now lies in data control, decision logic, risk governance, and margin defense amid automation.

Key forces:

- Embedded finance transfers risk to distribution points.

- Real-time systems unlock liquidity but heighten fragility.

- Modular stacks accelerate commoditization.

- AI reallocates margins probabilistically.

- Sustainability incentives (or lack thereof) shape outcomes.

Leaders who explicitly govern these shifts will dominate; those relying on innovation alone risk value leakage.

Table of Contents

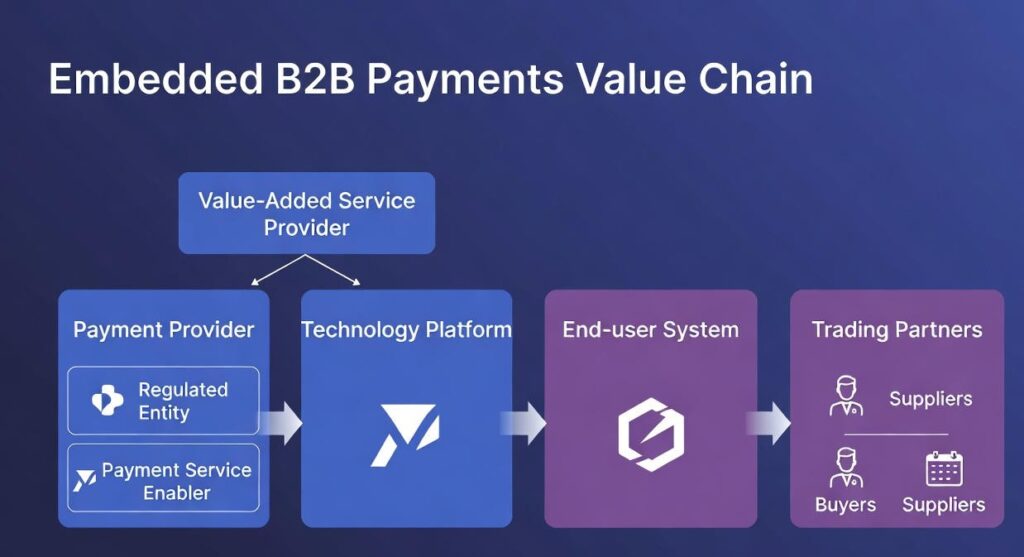

Embedded Finance: Not Just Growth—It’s a Risk Transfer Mechanism

Embedded finance integrates payments, lending, or insurance into non-financial platforms, often marketed as revenue upside. The reality: it accelerates risk transfer.

Platforms gain:

- Customer context and data ownership

- Pricing/product influence

Banks/PSPs retain:

- Balance-sheet and regulatory exposure

- Liquidity/settlement risk

As embedded B2B payments approach $16 trillion by 2030 (Edgar, Dunn & Company), platforms without risk discipline face amplified failures from instant credit and payouts.

Executive trade-off: Absorb complexity for customer proximity or insulate and cede value upstream. Neutrality isn’t possible.

Real-Time Payments: Unlocking Liquidity, Creating Shock Risks

Real-time networks alter cash flows profoundly. Upside: instant liquidity. Downside: eliminated float and controls.

Cross-border flows are projected to approach $290 trillion by 2030 (fintech reports). Errors propagate instantly.

Programmable money (tokenized deposits, stablecoins) adds rule-based automation—and brittleness. Agentic AI optimizes in real time, but blurs accountability.

Executive trade-off: Speed/automation vs. explainability/control. Legacy governance struggles with both.

Modular Architecture: Driving Agility, Accelerating Commoditization

API-first, composable payment stacks have replaced monolithic cores across much of the industry. New payment methods can be added in days. Fraud tools can be swapped without re-platforming. Regional compliance can be modularized.

Operationally, this is correct. Strategically, it is dangerous if misunderstood.

Modularity lowers switching costs—not only for providers, but for customers and partners. As orchestration layers abstract complexity, infrastructure differentiation erodes and pricing power follows.

Value migrates toward data ownership, intelligence, and control of decision logic. Many providers modernize efficiently, only to discover they have optimized themselves into interchangeability.

Executive trade-off: Build for agility and accept margin compression, or retain proprietary control and slow innovation velocity. This tension is unavoidable.

Modular Architecture: Driving Agility, Accelerating Commoditization

Composable, API-first stacks enable rapid additions and swaps.

Operationally ideal. Strategically perilous: lowers switching costs for all parties, eroding infrastructure pricing power.

Differentiation migrates to data, intelligence, and decision logic. Many modernize into interchangeability.

Executive trade-off: Agility with margin pressure vs. proprietary lock-in with slower velocity.

AI in Payments: Not a Feature—It’s a Margin Allocation Engine

AI drives 50-60% fraud reductions, compliance, and personalization.

Deeper impact: probabilistically prioritizes transactions/customers, reshaping economics without explicit oversight.

As decisions outpace human review, governance elevates to executive level.

Executive trade-off: Delegate for scale or oversee manually (add drag). Implicit choices are still choices.

Sustainability in Payments: Signals vs. Incentives

Initiatives like carbon-aware routing and tokenized green assets proliferate. Impact depends on embedding in economics (dynamic pricing, micro-incentives) vs. overlays.

Unsubstantiated claims invite scrutiny and liability.

Executive trade-off: Integrate now or remediate reputational/regulatory risk later

The Core Truth for 2025: Payments as Utility, Decision-Making as Differentiator

Mechanics converge; advantages endure in:

- Data/decision-logic control

- Scaled risk clarity

- Automation-paced governance

- Proactive margin confrontation

Innovation without control commodities. Winners master power dynamics as money outpaces organizations.

Disclaimer: This article reflects professional analysis based on publicly available information and anonymized industry experience. Views expressed are personal and do not constitute financial, legal, or investment advice.

Source: BCG, Paypers Report, Datalog, Coinlaw, BSMedia, Paymnts, edgar & dunn