The Enterprise Cross-Border Payments 2026 landscape is undergoing a structural transformation. The fragmented network of correspondent banks—once slow, opaque, and costly—is giving way to a unified, data-rich, and autonomous financial fabric. For CEOs and SVPs of Sales, the next 12 months are shaping up as a “Liquidity War,” where competitive advantage comes not from simply moving money, but from optimizing the intelligence and data surrounding every transaction.

Executive Summary

The Enterprise Cross-Border Payments 2026 landscape is undergoing a structural transformation. Key takeaways for CEOs and SVPs:

- Liquidity War: Optimize data and intelligence, not just money movement.

- ISO 20022: Unlock semantic data for AI-driven treasury and risk management.

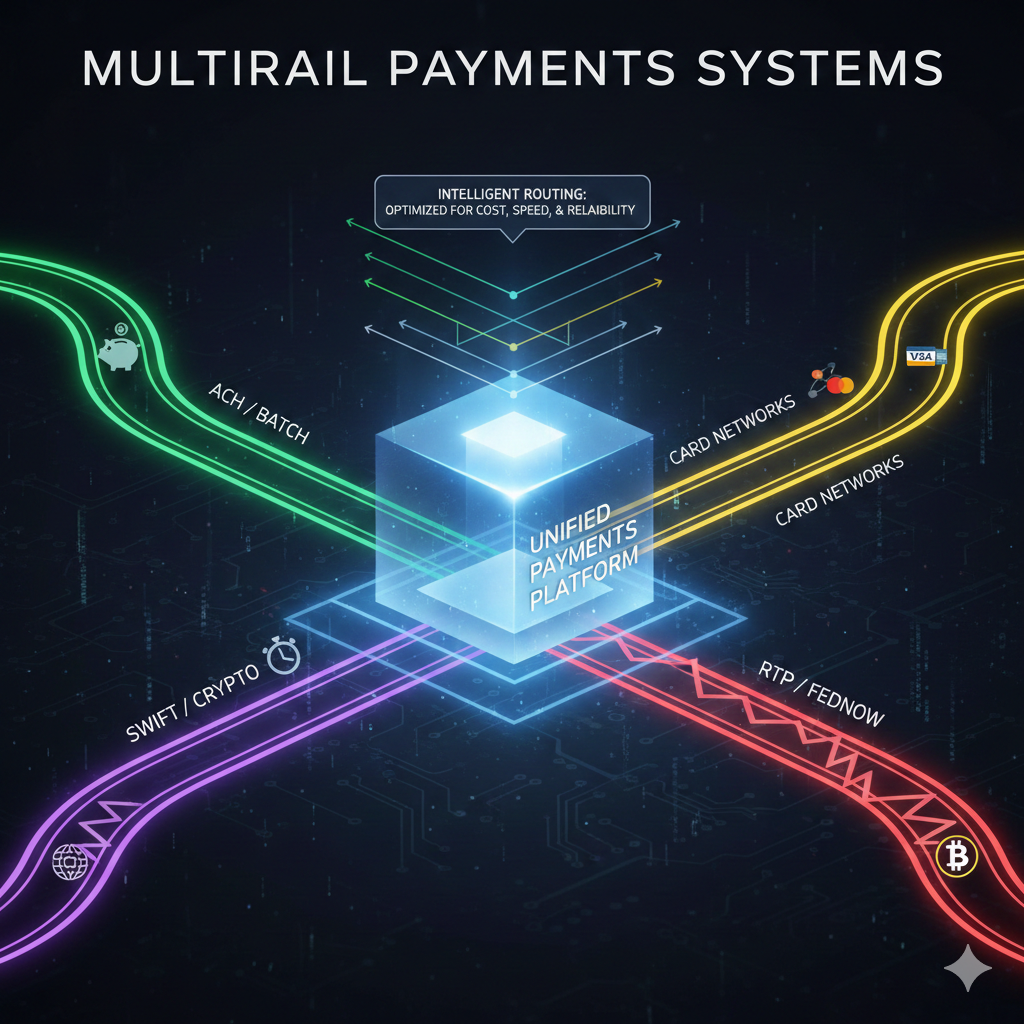

- Instant Rails: Connect domestic real-time systems (UPI, Pix, FedNow) into multilateral corridors.

- Stablecoins 2.0: Emerging as regulated B2B settlement rails with cost reduction potential.

- Agentic AI: Deploy AI agents for FX optimization, compliance, and Smart Acceptance.

- Regulatory Readiness: Embrace digital identity and Unified Trade Intelligence.

- Strategic Action: Weaponize data, integrate stablecoins, govern AI, align sales to payment strategy.