Multirail payment ecosystems are becoming the new operating system of global fintech as CXOs move beyond single-rail dependencies. Bold as many legacy-treasurers and CFOs may be, the era of a single dominant payment rail is over — and the real battleground will be defined by orchestration, not dominance. Real-time account-to-account (A2A) systems, diverse rails (cards, open-banking APIs, digital wallets, RTP networks) and AI-powered orchestration layers are converging. Boards that assume “cards + SWIFT = safe” are dangerously wrong. Here’s why most boards are getting this dangerously wrong — and what the top 1% are doing instead.

Executive Summary

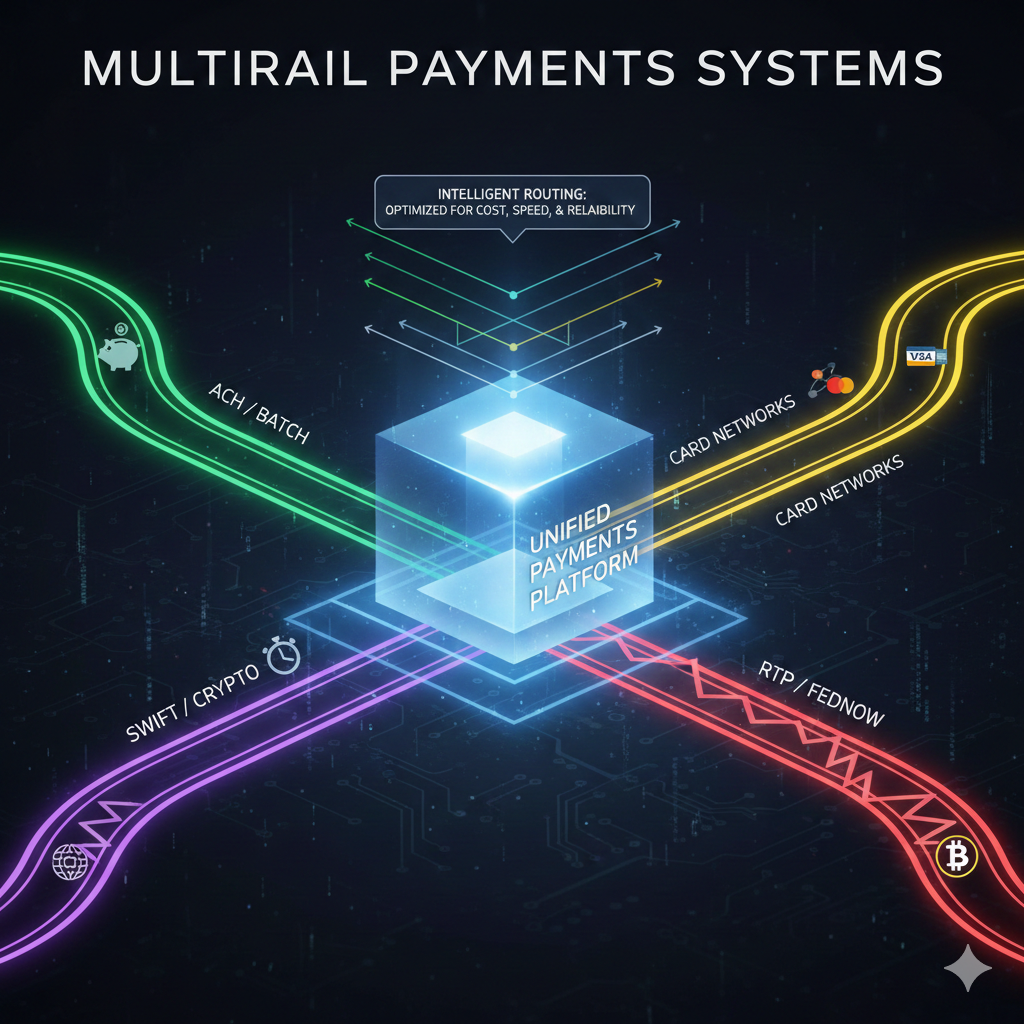

Understanding Multirail Payment Ecosystems

- Multirail convergence: A2A, real-time, cards, wallets — payment flows are fragmenting; orchestration is becoming the strategic asset.

- A2A explosion: Real-time A2A is growing globally — >70 countries now support RTP; volumes to double by 2028.

- Cost & speed advantage: A2A/instant rails threaten 15–25% of future card-transaction growth globally.

- Interoperability as growth lever: True value lies in cross-rail and cross-border interoperability; fragmentation is the principal bottleneck.

- AI-driven orchestration rising: AI routing and orchestration significantly reduce payment failures and improve efficiency.

- Compliance & risk as strategic constraints: Regulatory, liquidity, FX, and fraud-management complexity demand re-architecting.