In 2025’s compressing payments landscape—real-time rails eliminating float, AI surfacing risks instantly, embedded finance diluting margins, and ISO 20022 mandating richer data—credibility is the ultimate balance-sheet asset. Silent leadership (disciplined, low-ego execution) compounds it quietly. Leadership silence (avoidance disguised as caution) erodes it fatally. The executives who thrive will master the distinction: confront risks early and decisively, even when it costs short-term revenue.

Executive Summary

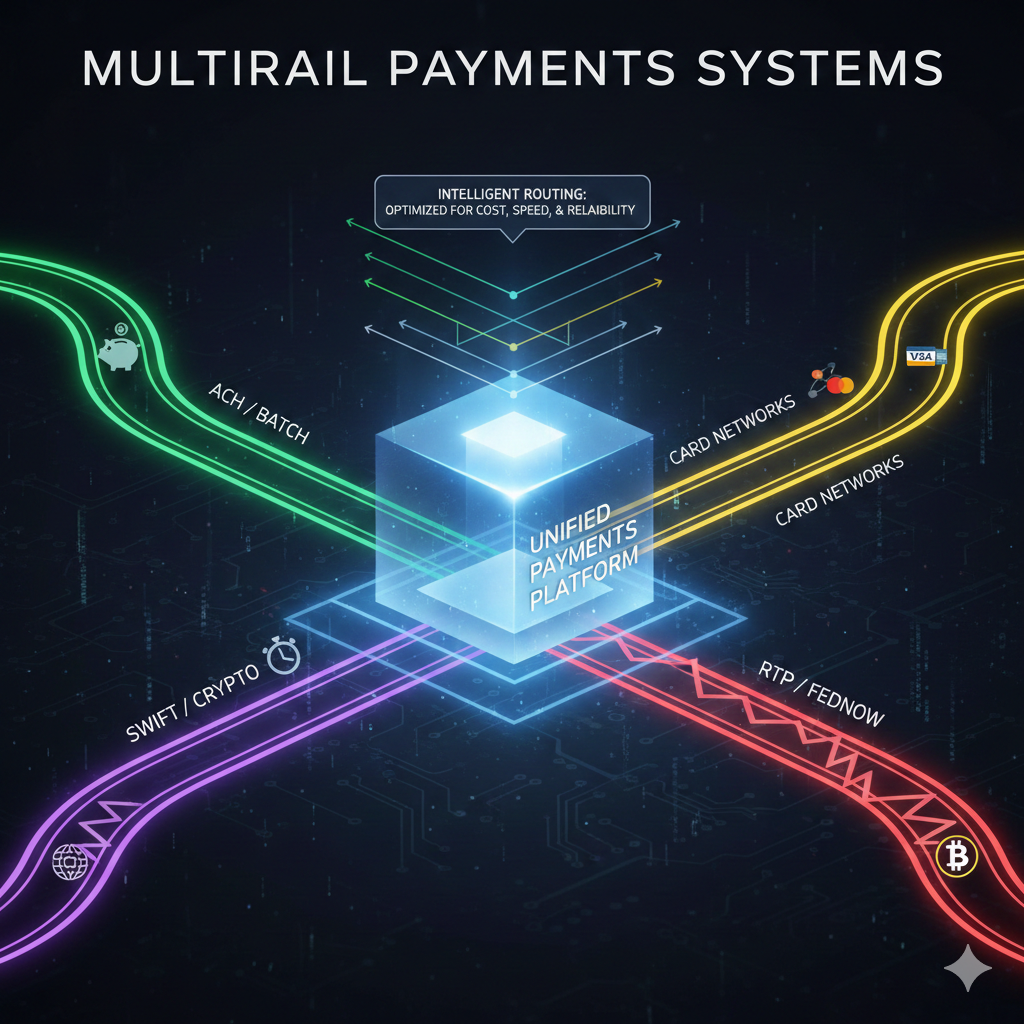

Global payments revenues hit approximately $2.5 trillion in 2025, processing trillions of transactions amid structural shifts: real-time payments surging (37% of merchants accepting them, with 80-90% expecting growth), ISO 20022 migration completing in November, AI-driven operations monetizing, and projected fraud losses climbing toward $400 billion cumulatively this decade.

Margins are under relentless pressure from embedded finance, instant rails, and competition. In this environment, leadership credibility—built through proactive risk confrontation and cultural resilience—determines who retains licenses, partners, and talent.

This piece contrasts silent leadership (aggressive internal action, public restraint) with leadership silence (deferred escalation on known weaknesses). The latter has fueled recent failures in bank-fintech models and fraud scandals. CXOs must audit unspoken risks now: silence is increasingly seen as intent by regulators and markets.